Finding the product in your platform

On the risks of over-emphasizing platform thinking

In an age of platform hype, everyone scrambles to find the platform in their product.

If you’re a product business, chances are you’ve been told that platforms beat products and hence you should look to become a platform.

There is a problem with over-emphasising platform thinking and the ‘platforms beat products’ narrative:

By positioning ‘platforms’ as superior to ‘products’, we risk throwing away the simple first principles of product thinking which have served us well for centuries.

We need to embrace ‘product thinking’ and find the product in our platform.

Understanding the ‘product’ in our platform helps us clarify where it really creates value, and more importantly, where it can effectively capture value.

Through the examples used below, it will also help understand:

How Spotify gains control back from labels

Why most Banking-as-a-service API platforms fail

Where reputation systems work and where they don’t

Why food delivery models work better in Asia/LatAm than in Europe/US

Amazon’s right to play in the Kindle publishing ecosystem

Let’s dig in!

What is a product, really?

Traditional product value chains operate across inputs, product, and distribution.

This simple arrangement creates a linear flow of value to create -what I first called back in 2013 - a ‘pipe’ or a ‘pipeline’.

A product is the offering the firm creates through the transformation of inputs, which it then distributes downstream.

This is fairly straightforward in product value chains.

It gets a lot more vague with platforms.

Platforms combine:

a mechanism to attract and organize inputs (on the producer side) and

a mechanism to distribute (on the consumer side).

But what is the ‘product’ in the middle in case of platforms.

Essentially, apart from aggregating and organizing producers and consumers - which is largely a mechanism to organize value chain actors - what is the unique product that the platform is creating which gives it the right to sit at the centre of the ecosystem?

If you think of it, distributors and brokers also aggregate producers and consumers. Yet they don’t command the right to sit at the centre of the ecosystem (except through the control of asymmetric information or relationships).

The ‘product’ creates the difference between a distributor and a platform.

What is a platform uniquely creating in the middle which gives it the right to sit at the center of the ecosystem?

Let’s unpack this with a few examples.

If you can accurately identify and explain the product in your platform, you will have a much better handle of your right to play as a platform business.

The ‘product’ in Spotify’s platform

What does Spotify really ‘produce’?

You might say that Spotify’s product is the music streaming service. But that’s really just a proprietary distribution technology in a product value chain.

You might argue that the products are the songs. But that’s not what Spotify is really producing. The labels own the songs, the artists create them. The songs are inputs into the ‘production’ process.

What exactly is the ‘product’ in Spotify’s platform?

Spotify’s ‘product’ is the playlist.

Playlists are central to Spotify’s strategy within the music ecosystem.

Songs, which were traditionally bundled into albums, were unbundled by the internet and then went through three phases of

free distribution through file-sharing services like Kazaa and Napster,

pay-per-tune distribution through iTunes, and

fixed-fee unlimited catalog distribution through Spotify.

This unbundled song distribution changed for the first time with Spotify’s playlists.

Playlists provide the locus of rebundling where songs - unbundled from albums and artists - are rebundled into theme-based playlists.

As WIRED points out:

Playlist placements are highly coveted, both for how they rack up the streams and the way they expose music to new listeners.

Indeed, playlists have become so important that being left off can flop even megastar releases (as Katy Perry discovered after Spotify blackballed her for giving rival Apple Music a temporary exclusive, reminiscent of Amazon cutting off publishers who wouldn’t give it big enough discounts).

Playlists are the core product driving discovery of new artists. They are critical for Spotify to gain a right to sit in the middle of the music value chain and not be merely a digital distributor for the top 3 music labels.

What Spotify ‘sells’ to advertisers and brands is influence and targeting through playlists.

The “Sponsored Playlist” program allows brands to sponsor a Spotify-curated playlist for 1 week.

Using the metadata of playlists, Spotify also launched “Branded Moments,” a program which leverages the real-time insights playlists offer into activities that listeners are engaged in. E.g. a fitness brand targeting a playlist labeled Workout.

The playlist - the central locus of rebundling in the music streaming business - is Spotify’s core product.

Spotify takes songs/tracks as ‘inputs’, rebundles them into playlists as ‘product’, and sends them down its proprietary streaming ‘distribution’ channel.

And all of this helps Spotify gain power back from the labels.

Without the playlist, Spotify is merely a glorified distributor in the music value chain. A scaled out one, no doubt, but at the end of it all, just a glorified distributor dependent on the whims and fancies of a highly concentrated supplier base constituting three music labels.

The playlist is the ‘product’ that gives Spotify the right to be a platform.

The ‘product’ in Airbnb’s platform

What’s the ‘product’ in Airbnb’s platform?

In high-risk markets like short-term accommodation, trust is unbundled and dispersed across market transactions. Establishing trust requires peer-to-peer tools without central mediation. This may involve

individual negotiations,

reputation-building (and subsequently relationship building) over time, or

reliance on friends-of-friends recommendations (a form of transitive trust where A trusts B and B trusts C so A trusts C).

Platforms step in to rebundle trust, which is otherwise embedded in these personal relationships.

In doing so, the platform creates its core product - a mechanism for imputing trust into market transactions.

Instead of relying on fragmented, individual trust-building processes, the platform ‘produces’ a centralized market-wide ‘product’ for establishing and verifying trust.

Airbnb’s ‘product’ - the real value driver for which it can charge a premium on market activity - is its reputation system.

The reputation system is built off explicit inputs like user ratings and implicit signals like cancellation rates after check-in. It manifests explicitly in the form of a five star rating on the interface and implicitly in the exposure/ranking that a listing gets in search results.

The reputation system is the product created at the point of rebundling.

Users pay a premium for the assurance and reliability provided by this ‘product’. Users can engage in transactions with a higher degree of certainty, knowing that trust is not scattered but centralized and managed through the platform's infrastructure.

The product in your platform sits at the point of rebundling

What exactly are we talking about here?

The ‘product’ within a platform is created at the point of rebundling.

As digital technologies drive organizations and markets towards unbundling, platforms create value not just through mere integration and aggregation…

…but through rebundling.

This is why vertical marketplaces repeatedly attack Ebay and Craigslist. Horizontal marketplaces win through mere integration and aggregation but they remain vulnerable to attack from a player that doesn’t just aggregate vertical inventory but also creates a superior vertical ‘product’ to organize that market.

What creates a compelling ‘product’ on your platform?

A platform’s goal is to create an efficient market by reducing transaction costs. The ‘product’ in your platform is the unique innovation you provide to solve that problem.

A platform business is not just an open organizational infrastructure but a space where rebundling creates new value. The platforms that win are best able to create relevant products at the point of rebundling.

In fact, let’s clarify this with a few more examples.

The product in Kindle’s platform

What’s the ‘product’ in Kindle’s platform?

Again, books are inputs into the self-publishing value chain, so what is the ‘product’ that Amazon creates?

You’d be tempted to say that the physical reading device - the Kindle - is the product. That’s partly correct. The Kindle reader did introduce innovations like the e-ink electronic paper, which transform the reading experience.

But the Kindle is primarily a proprietary distribution channel, performing the same role that Spotify’s streaming technologies play. That is why it is subsidized and sold at a really low price.

So what exactly is the ‘product’ that Amazon is creating between the inputs of books and the proprietary distribution of Kindle.

Amazon’s ‘product’ is the community of book reviewers that Amazon has built up over time.

Hang in there while I unpack this: we’re not saying that the reputation system itself (as was the case with Airbnb) is Amazon’s ‘product’.

No!

To be very precise, Amazon’s production in the e-book value chain - its unique value-adding contribution beyond shaving off distribution costs - is the creative capacity of its community book reviewers.

Book reviews are critical to discovery of new books, particularly by first-time authors. But creating a robust book review and rating system is non-trivial. Unlike most product reviews, useful book reviews require significant investment of time and effort on the part of the reviewer. Hence, curating a community of book reviewers is non-trivial.

Traditionally, the large publishing houses bundled

(1) the ability to publish and distribute books, and

(2) through their PR arm, the ability to generate book reviews with media houses.

Even before the rise of the web, but particularly after it, book reviews started getting unbundled as peer-to-peer recommendations via email lists, and subsequently via blogs and social media.

Book reviewers were scattered across the web. Amazon - by establishing itself as the single place online to buy books - attracted a community of book reviewers.

Amazon curated this community of book reviewers leveraging supply of traditional published books from the large publishing houses. Leveraging this growing community of book reviewers, Amazon established itself as the point of rebundling of book reviews.

Once it had created this new locus of rebundling of book reviews in the value chain of traditionally published books, it then moved this ‘product’ into a new value chain - the value chain of self-published e-books.

This transition is crucial. Amazon needed to play in the traditional publishing value chain to attract a curated community of reviewers which it then transferred to the self-publishing value chain. By combining the ‘curated community of reviewers’ with its proprietary distribution mechanism, Amazon established a chokehold over the self-publishing value chain.

Readers looking for new indie writing look to Amazon and its curated base of reviewers for guidance. For authors, it is far more effective to rack up reviews on Amazon than to work with hundreds of unbundled blogs and influencers.

The core ‘product’ establishes Amazon firmly at the centre of the self-publishing value chain.

The ‘product’ as new value created by the platform

The best way to understand the product is to look at Spotify's playlist. Arguably, the user’s need of 'help me find a song to listen to' is already solved by Spotify's search function.

The playlist does something else. It helps Spotify create a new dynamic for music discovery and gives it the right to sit at the center of the music value chain having created new value.

Amazon's book reviewers play a similar role. A search box is sufficient to help consumers fulfil their need and find books. But the platform creates a 'product' in delivering the ability to help unknown authors get rediscovered. That is a unique ‘product’ that is not available elsewhere and is not created through mere aggregation of inventory.

This is the key idea of finding the ‘product’ in your platform.

The product in food delivery platforms

Let’s look at food delivery platforms. What’s the ‘product’ here?

Having just looked at Airbnb and swayed by the ‘sharing economy’ catch-all phrase, you might be tempted to say it’s the driver and/or restaurant reputation system.

But you’re not really engaging in market transactions based on driver reputation and restaurant reputations, while somewhat important, do not determine the key vector of consumer experience in food delivery.

To identify the core ‘product’ in food delivery, let’s turn on the unbundling-rebundling lens again.

Restaurants that would manage their own food delivery would bundle food preparation and food delivery.

Food delivery platforms unbundle food prep from food delivery and rebundle food delivery using a near-captive base of delivery agents.

In doing this, these platforms gain a unique advantage over individual restaurants that managed their food delivery. They set up a market-wide data value chain where they gather demand data across the market and transform it into their core product: route optimization and delivery stacking algorithms.

Route optimization and delivery stacking, particularly in high-density cities in Asia and LatAm, enables food delivery platforms to differentiate on faster deliveries and gain a right to sit in the middle.

Food delivery platforms which decide to backward integrate into creating ‘dark kitchens’ create another important product: the standardized minimal menu of the dark kitchen. Demand data captured at market-wide scale informs these platforms of (1) what’s popular, (2) where it’s ordered from, (3) order patterns. These three data types help determine (1) location of ‘dark kitchens’ to minimize delivery times, (2) menu, and (3) estimates for ingredient sourcing and food production.

There’s an important nuance here. The product of the ‘dark kitchen’ is the food that’s created but the ‘product’ of the food delivery platform is the standardized minimal menu (what to produce) and the production schedule (when to produce), both of which are built off the market-wide data gathered by the platform.

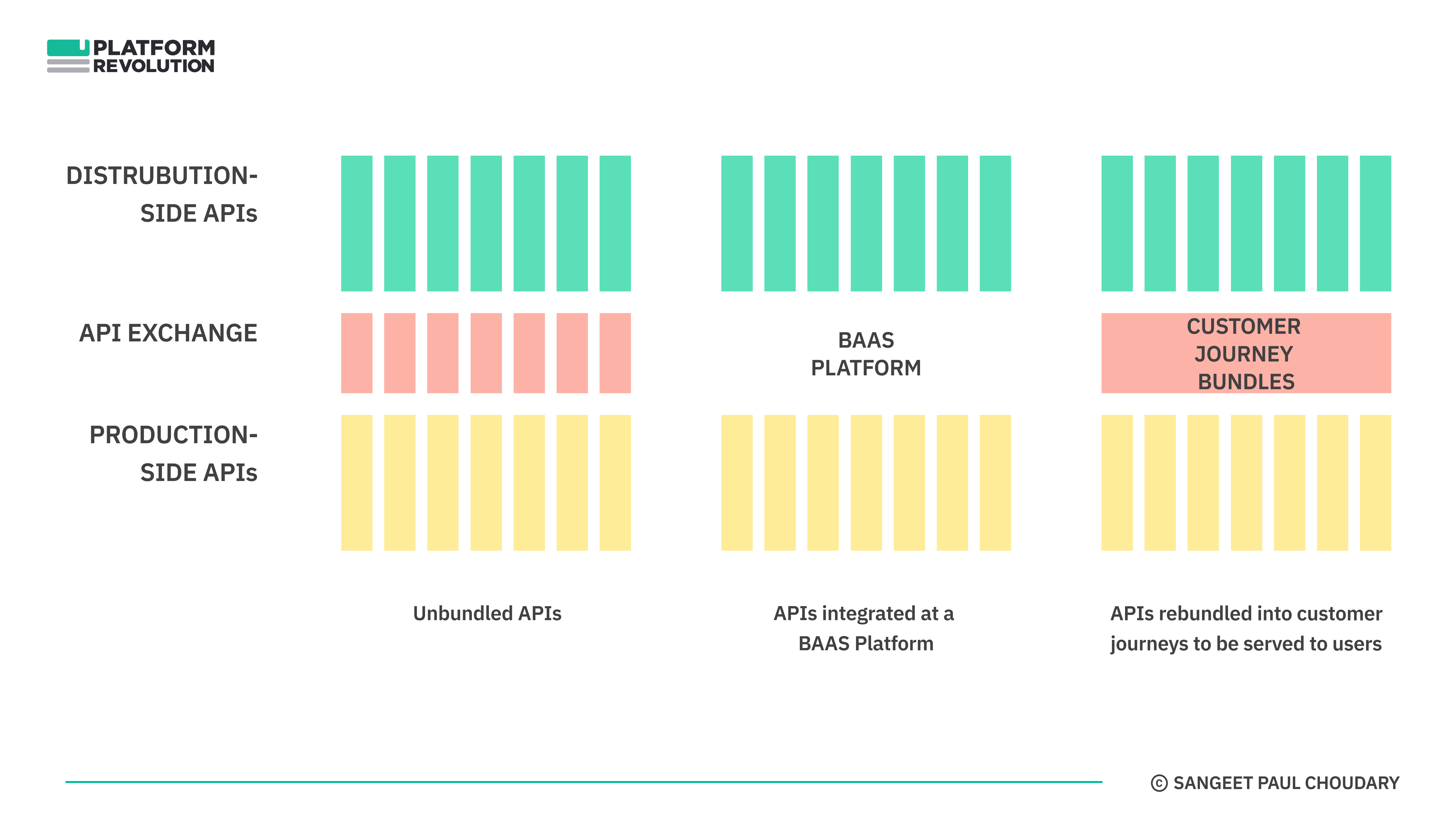

Why most Banking-as-a-service platforms fail

Let’s look at a counter example.

As firms increasingly open up APIs, business capabilities are being unbundled from organizations and are opened out to be rebundled externally into new products.

Take the financial services landscape as an example. As I point out in The financial services value stack:

The ability to modularize and provision financial services as APIs enables unbundling and rebundling in the financial services industry.

The API exchange layer (typically referred to as Banking-as-a-service platforms) manages interactions across the financial services stack. On one hand, this layer aggregates product provisioning APIs across the financial services production ecosystem. On the other hand, it integrates across websites, apps, and other digital services in the consumption ecosystem, providing them access to these APIs.

With every bank provisioning its product as APIs, players at the API exchange layer manage the aggregation and provisioning of these APIs across multiple banks.

This sounds simple enough. Aggregate production side APIs (inputs) on one side and integrate with consumption-side APIs (distribution) on the other, and create a one-stop integration layer.

Yet, most Banking-as-a-service (BAAS) platforms fail.

Neither the inputs nor the distribution are proprietary. Any substitute integration layer can also aggregate the same APIs.

The BAAS platforms that eventually win are the ones that are able to create ‘products’ at the point of rebundling. These ‘products’ are carefully crafted consumer journeys, typically created by:

taking production-side APIs as input,

wrapping them in core banking capabilities to make the APIs consumable by third-party non-banking entities, and

rebundling them into a consumption-side customer journey.

BAAS platforms win when they develop deep customer insight into consumption-side journeys at their partners (e.g. buyer journey at an e-commerce store) and carefully curate the most relevant production-side APIs into that bundle.

BAAS platforms that do not create these ‘products’ fail.

The ‘product’, again, is created at the point of rebundling and give the platform the right to site in the value chain beyond being a market-wide integrator and distributor.

The not-so-obvious ‘product’ in your platform

You would have figures by now that to really get to the ‘product’ in your platform you need to reason with first principles, not with analogy.

As an example, Amazon Kindle Publishing, Airbnb, and Meituan/Grab/Zomato - all use reputation systems. Yet, the ‘product’ in their platforms isn’t uniformly the reputation system.

To get to the ‘product’ in your platform, try to identify the key vector of differentiation. For the three platforms above, this translates to:

Airbnb: Assure me of a safe stay

Amazon: Help me find a good book by an unknown author OR Help me get discovered as an unknown author

Meituan: Help me get my food as soon as possible.

Note that this isn’t just the overall consumer problem. E.g. there’s a difference between ‘help me find what I’m looking for’ and ‘help me find a good book by an unknown author’. The first can be solved through aggregation alone, the second needs curation and rebundling.

Back to the three scenarios above… All three have reputation systems, yet reputation is not a key performance vector for Meituan. Delivery times - and, hence, route optimization and delivery stacking - matter more.

Between Amazon and Airbnb, the reputation problems are fundamentally different. The risk of a bad transaction is much higher on Airbnb (host physically harms you) than on Amazon (you read a crappy book). Reputation is, hence, the key performance vector in centralizing trust and delivering a safe market.

On the other hand, the reviewer base on Amazon plays a crucial role. First, unlike TikTok videos and Tinder swipes, where you can provide feedback on content instantly, reviewing books requires significant investment in reading the book. Gathering the right reviewers together who are keen to sample new books is far more important than just getting to scale with a rating system.

As the examples demonstrate, the ‘product’ in your platform will be determined by the key performance vector at the point of rebundling.

Two very similar platforms may have fundamentally different core ‘products’ based on the nature of their value chains and the specific role the platform performs within it.

Finding the product - why it matters

This post isn’t meant as a prescription, it’s meant to provoke debate.

Over the past decade, I’ve advised a very wide range of platform initiatives.

And I repeatedly see one issue emerge.

Business leaders are more focused on debating openness and finding new user bases and third parties to connect in to check the “Are-we-a-platform” checkboxes, than they are on clearly articulating why a platform is needed in the first place.

In essence, they’re more obsessed with finding the platform in their product than they are in determining whether there really is a product in the platform they are trying to build.

What’s the unique value created by the platform beyond merely bringing together demand and supply?

This is where it helps to take off the fancy platform thinking buzzwords and go back to the first principles of looking at your platform business as you would look at any business i.e. look for the ‘product’ in your platform business.

Don’t get me wrong - I love platform thinking - I literally wrote the book on this topic and have built more than a decade of work advising businesses and regulators on this topic.

But every so often, it’s important to come back to look not at what’s changing but what remains the same.

The central idea of a product in a value chain doesn’t go away with a change in business model. It’s a lot less clear what the core product is in a platform business model, but that’s precisely why clarifying it is all the more important.

I hope you’ve enjoyed reading this piece. If you’d like to kick these ideas around some more, feel free to leave a comment below.

Hi Sangeet.

Great distinction. Yes, everyone wants a platform, but there's more work to do.

As you distinguished aggregation vs production (un- and re-bundling), I thought about Joe Pine/Jim Gilmore's evolution of value (and production) from goods to services to experiences to personal transformations. The Spotify, AirBnB, and Kindle case studies deliver digitized/physical experiences enabled by digital meta-data. The Food Delivery Platform is a service (improved by digitization) with bonus unbundled elements of its value chain. Each has its competitive profile.

Perhaps your other essay on generative AI (I haven't delved into it yet) falls in the transformation zone since it fits into the futurist computer scientist's "tools for thought" vision of augmentation.

Love your thoughts! Rob

Great read. Thank you for all the examples which do as you say, really help bring the ideas to life.