Spotify, connected cars, and open banking - Platforms or glorified distributors?

Gaining power in concentrated markets

What do Spotify, the connected vehicle data market, open banking APIs, and trade finance blockchain projects have in common?

All of these involve markets where power is concentrated among a few producers.

A handful of music labels own 70% of the music industry’s licensing rights.

A handful of vehicle manufacturers dominate the connected vehicle data industry in most vehicle segments.

Intermediaries who step in to organize such markets may claim to be platforms but they usually end up just acting as glorified distributors.

Even in the financial services industry in some countries, a handful of banks provision most of the financial services. Banking-as-a-service (BAAS) ‘platforms’ end up merely acting as glorified distributors. We see this play out in the connected home market, traditional energy markets, healthcare markets, and many others.

In such markets, power accrues not to the so-called ‘platform’ intermediary but to the producers.

How exactly do you play in such markets to shift power back to yourself as an intermediary?

How do you move from being a glorified distributor to setting up a core platform position?

Let’s dig in!

Spotify: Platform or glorified distributor?

Spotify today accounts for more than a quarter of global recorded music revenues. In contrast, the iTunes Music Store accounted for less than 10% of total revenues in the pre-streaming years.

Despite its dominant market position (by numbers) it has a weak position in the music value chain.

The recorded music value chain skews in favour of the owners of music copyright and license - the record labels.

Here’s what that concentration looks like: The three major music labels control nearly 70% of global recorded music revenues and account for more than 80% of all the music streamed by users.

This concentration upstream essentially shifts power away from the intermediary.

Intermediaries gain power by organizing unorganized markets. Airbnb’s technology - particularly its trust system - is aimed at organising an unorganized market by imputing trust to transactions.

In contrast, Spotify’s technology is primarily aimed at simplifying consumption through streaming.

Spotify - by most accounts - is merely a glorified distributor in the music value chain.

How does Spotify wrest power back?

Gaining power in concentrated markets

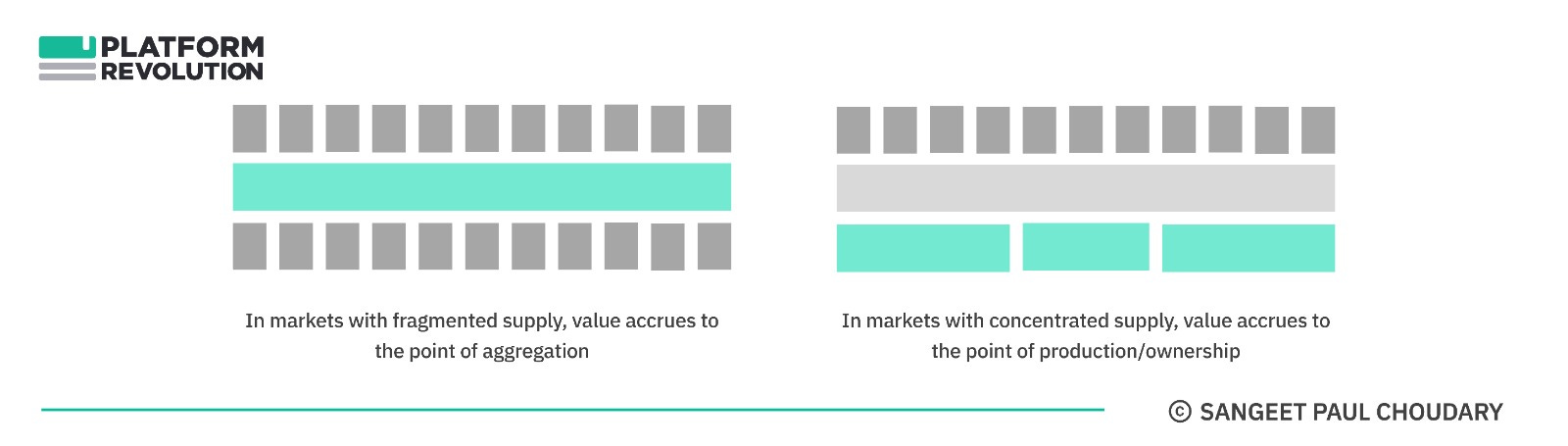

The dominant narrative in the platform economy is that power accrues to the point of aggregation i.e. the platform.

This is true, but only in markets where supply is highly fragmented. The more fragmented the supply, the lower its negotiating power, and the greater value created for consumers through aggregation.

However in markets with concentrated supply, power skews towards the producers and/or owners of supply.

In these markets, intermediaries are mere distributors. Consumers don’t incur significant search costs and hence no real value is created through aggregation.

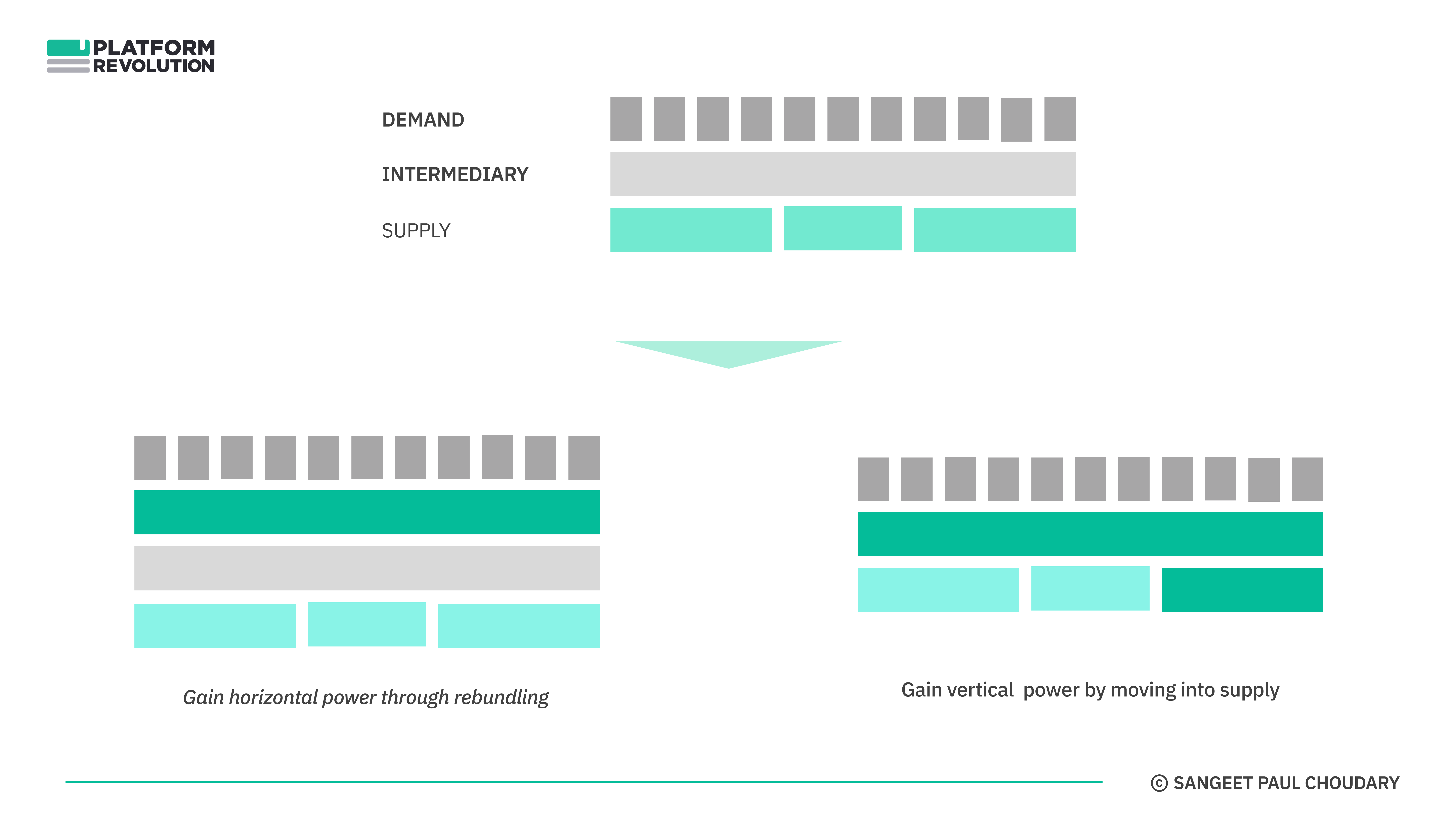

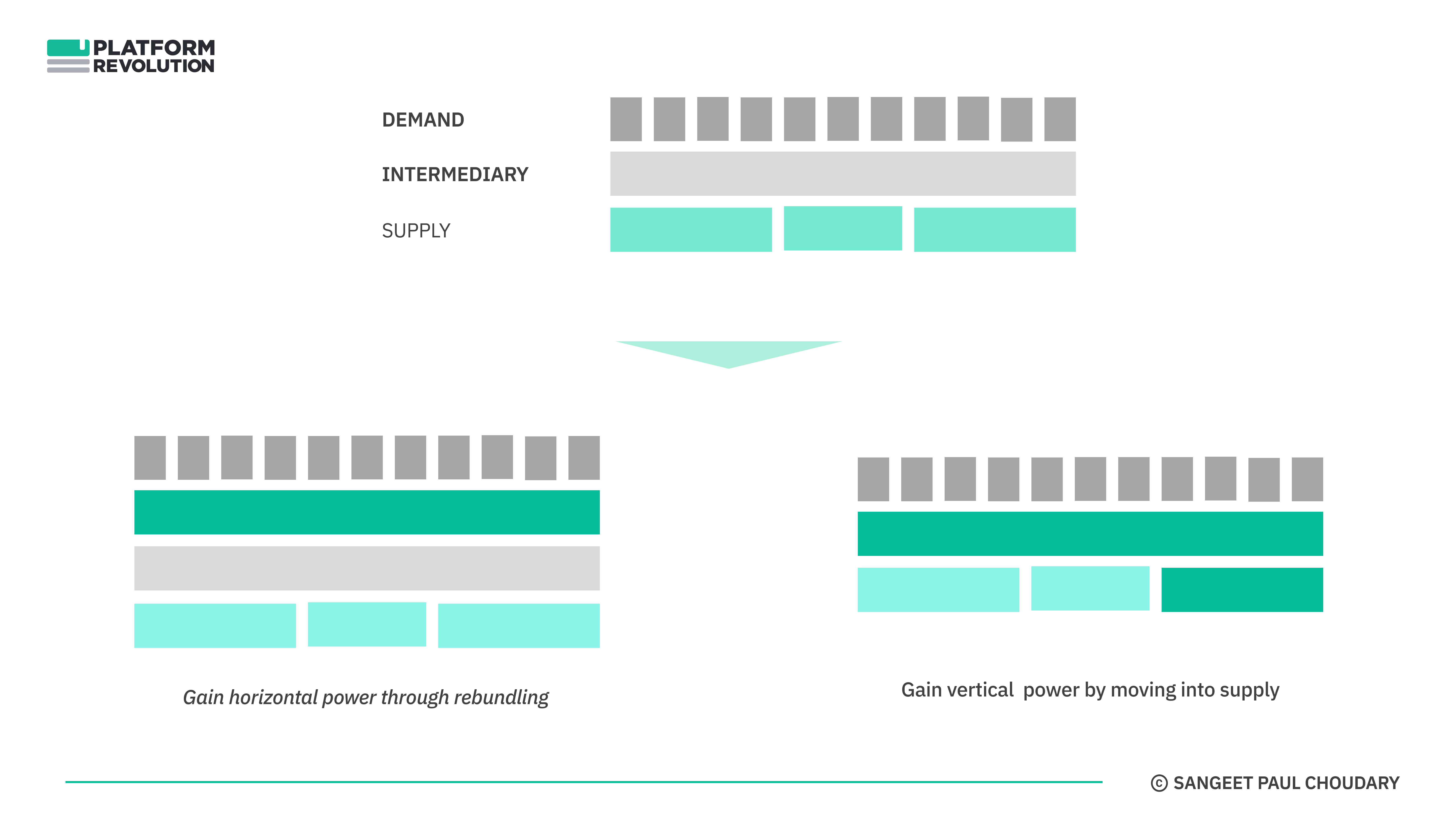

In such markets, there are two ways that the intermediary can wrest power back towards itself:

The intermediary can develop horizontal power by rebundling inputs from suppliers into proprietary new bundles

The intermediary can leverage data about the end users, an advantage it has over producers, to backward integrate into production.

Building vertical power

Building vertical power is a more obvious approach so let’s get that out of the way first. Netflix is a great example of a company that’s followed the second strategy of building vertical power.

Working in a market dominated by a few large production houses, Netflix developed a data advantage, first through its DVD rental business and then through streaming itself.

As I explain in Why offline retailers fail at online marketplaces, access to demand-side data is a critical source of advantage for any intermediary. Even Netflix’s DVD rental business could better manage inventory because of its superior access to demand-side data:

The one thing that Blockbuster could never compete with was the integration of demand-side queuing data (users would add movies that they wanted to watch next into a queue) with a national-scale logistics system. All this queueing data aggregated at a national scale informed Netflix on upcoming demand for DVDs across the country.

Blockbuster could only serve users based on DVD inventory available at a local store. This resulted in:

1) low availability of some titles ( local demand > local supply), and

2) low utilization of other titles (local supply > local demand).

Netflix, on the other hand, could move DVDs to different parts of the US based on where users were queueing those titles. This resulted in higher availability while also having fewer titles idle at any point.

Netflix had already built a treasure-trove of data through its DVD rental business alone. With streaming, it was able to push this several notches further looking at which segments of which movies were skipped, rewatched etc to develop fine-grained profiles of customer viewing habits.

This data advantage allows Netflix to drastically improve returns on innovation.

Building horizontal power

This bring us back to Spotify.

To gain power back from labels, Spotify has been pursuing both horizontal and vertical strategies.

The vertical strategies are best seen in its moves into podcasting where it can control the entire value chain (paying Joe Rogan and other huge sums to acquire their content).

But Spotify provides an even better example of developing horizontal power through rebundling.

As I explained in Finding the product in your platform:

Playlists are central to Spotify’s strategy within the music ecosystem.

Songs, which were traditionally bundled into albums, were unbundled by the internet and then went through three phases of

free distribution through file-sharing services like Kazaa and Napster,

pay-per-tune distribution through iTunes, and

fixed-fee unlimited catalog distribution through Spotify.

This unbundled song distribution changed for the first time with Spotify’s playlists.

Playlists provide the locus of rebundling where songs - unbundled from albums and artists - are rebundled into theme-based playlists.

Spotify’s playlists are critical to developing horizontal power in the music value chain.

With greater power comes greater monetization. And rebundling is central to pursuing monetization.

Monetizing music

Here’s an open secret:

The only players who make money with music are the labels.

And Taylor Swift!

That’s about it. No one else makes money with music. Not the artists, not the retailers, not the streaming platforms.

In fact, everyone else makes money by commoditizing music and creating gatekeeping power.

iTunes created a business model around unbundling the album. But iTunes monetization was never about making money with music, it was more about creating a high-priced consumer electronics product with low-priced complements (unbundled songs), a strategy it has successfully ported to the iPhone App Store as well.

Apple commoditized music to make a music-playing device valuable. A Sony walkman playing an album ‘bundle’ can never capture profits the way an iPod playing the unbundled album can. Apple’s strategy has never been to accrue value to the music or app market but to commoditize those markets and accrue value to its consumer products.

Unlike other content markets, where platforms monetize through their gatekeeping power, controlling access to consumers, Spotify has no gatekeeping power. The labels control the point of gatekeeping.

Spotify has known this all along. As a glorified distributor, it can at best gain distributor margins. Traditional pipeline-world distributor margins are nothing to get excited about, even at global scale.

And that’s where Spotify’s playlists help to create gatekeeping power where none exist.

Spotify leverages playlists as both a distribution chokepoint for artists and as advertising real estate for brands.

Migrating value with playlists

Playlists serve as a new locus for negotiating power within Spotify's ecosystem.

Spotify exercises curation control - both editorially and algorithmically - to decide which songs and artists are included in its playlists.

Spotify also pushes playlists as the primary mechanism through which users consume music. By pushing playlist-based consumption Spotify inserts itself into a new position in the value chain. Songs and artists which are featured on playlists end up getting far greater exposure.

Without playlists, Spotify has very limited gatekeeping power. It is merely a distributor with a search function.

Playlists change that power equation.

Technically, anyone can create a playlist. But technical rights don’t necessarily translate to market access.

Spotify-created playlists invariably have far greater distribution power than user-generated or label-owned playlists. Almost all the top most followed playlists on Spotify are neither user-generated nor label-owned. They are Spotify-created playlists.

Artists looking to be featured on top playlists are hostage to Spotify’s curatorial power through its playlists.

Spotify also actively demotes third-party-created playlists and features its own. All these moves are afforded by the central curatorial power of playlists.

Channelling music consumption through playlists has a lot of the power dynamic that radio did, where consumers would listen to whatever the Radio Jockeys decided to play, except that instead of RJs taste-making on a local radio network, you now have a single dominant RJ at global scale.

Research at the NBER shows that getting featured on the right playlists is critical to artist discovery (and hence streams and earnings) on Spotify.

The research highlights that adding a track to the “Viva Latino!” playlist could generate between US$303,047 and US$424,265 in added revenue per track. The closer the track was featured to the top of the playlist, the greater the impact on revenues.

Spotify’s screen real estate determines winners and losers in the music industry.

Playing power games with rebundling

The centrality of playlists to Spotify’s strategy illustrates an important point.

You gain power in concentrated markets through rebundling.

Unbundling fragments power. Bundling concentrates power.

Without rebundling songs into playlists, Spotify is merely a distributor.

Bringing demand and supply together isn’t sufficient. Even distributors and retailers act as aggregation points for demand to meet supply.

In order to create a powerful position in the middle, intermediaries in fragmented markets need to create new value through rebundling.

Rebundling can help shift power in the direction of the intermediary (and away from the producer) if consumer attention skews towards the new bundle.

There’s an important nuance here. I’m not suggesting that consumers need to value the new bundle more. Spotify’s consumers do not necessarily value playlists more than the traditional search paradigm or merely listening to their favourite artists. But Spotify’s interface pushes playlists front and center, which helps skew consumer attention towards playlists.

As I’ve noted before in Finding the product in your platform, this essentially involves creating a new locus of rebundling:

As digital technologies drive organizations and markets towards unbundling, platforms create value not just through mere integration and aggregation…

…but through rebundling.

A platform business is not just an open organizational infrastructure but a space where rebundling creates new value. The platforms that win are best able to create relevant products at the point of rebundling.

In the case of Spotify, this translates to the idea of playlists.

Playlists are the central weapon in Spotify’s arsenal in their fight against the labels.

Rebundling on platforms creates a locus of power by enabling platforms to strategically coordinate between multiple markets and actors, thereby exerting influence and control.

Power games in vehicle data markets

Vehicle data markets have a similar power structure. A few producers of vehicle data - large automotive manufacturers - control all vehicle data and the resultant power across the value chain.

Vehicle data hubs have emerged as a popular business model since the mid-2010s. Since every automotive manufacturer has their own data format and access, vehicle data hubs provide a central point of access across all vehicles and standardize data formats and access terms.

They raise capital telling a story about how they’re a platform play.

But as you’d have figured by now, vehicle data hubs aren’t really platforms, they are glorified distributors or data brokers.

As I explain in Switchboard strategy:

The automotive industry's consolidated industry structure skews power away from Otonomo and in favour of the OEMs which act as production partners. As a result, even though Otonomo runs an integrator business model, it gets automotive OEMs on board as a data broker, managing their data and driving adoption of this data across the distribution ecosystem, which constitutes app developers who build connected car applications.

In order to gain power away from the OEMs, these vehicle data hubs need to attract new innovation and rebundle vehicle data into entirely new data products and applications that individual vehicle manufacturers would struggle to create.

This is where demand-side data becomes a crucial source of power.

Rebundling is achieved through demand-side data

What gives the intermediary the right to rebundle? What does the intermediary have that the producers or owners of supply do not?

Access to demand-side data delivers the right to rebundle.

This goes back to Netflix and the point about building vertical power.

Much like vertical power is gained through access to demand-side data, horizontal power of rebundling is also created through access to demand-side data.

If the intermediary understands demand patterns which producers do not, it can take inputs from the producers and rebundle them into consumer-centric bundles on the demand side.

We see this play out with Spotify’s playlists. And we see this play out in financial services too.

How to win at open banking

Let’s talk about open banking.

The banking industry is fairly concentrated in some countries. When a few banks concentrate deposits (and lending), their APIs also become most sought after as their financial products often offer the best terms.

Similar power games emerge. A few banks dominate the open API production landscape.

As banks open out APIs, ‘intermediaries’ emerge to integrate across these APIs and provide a one-stop integration point for the industry.

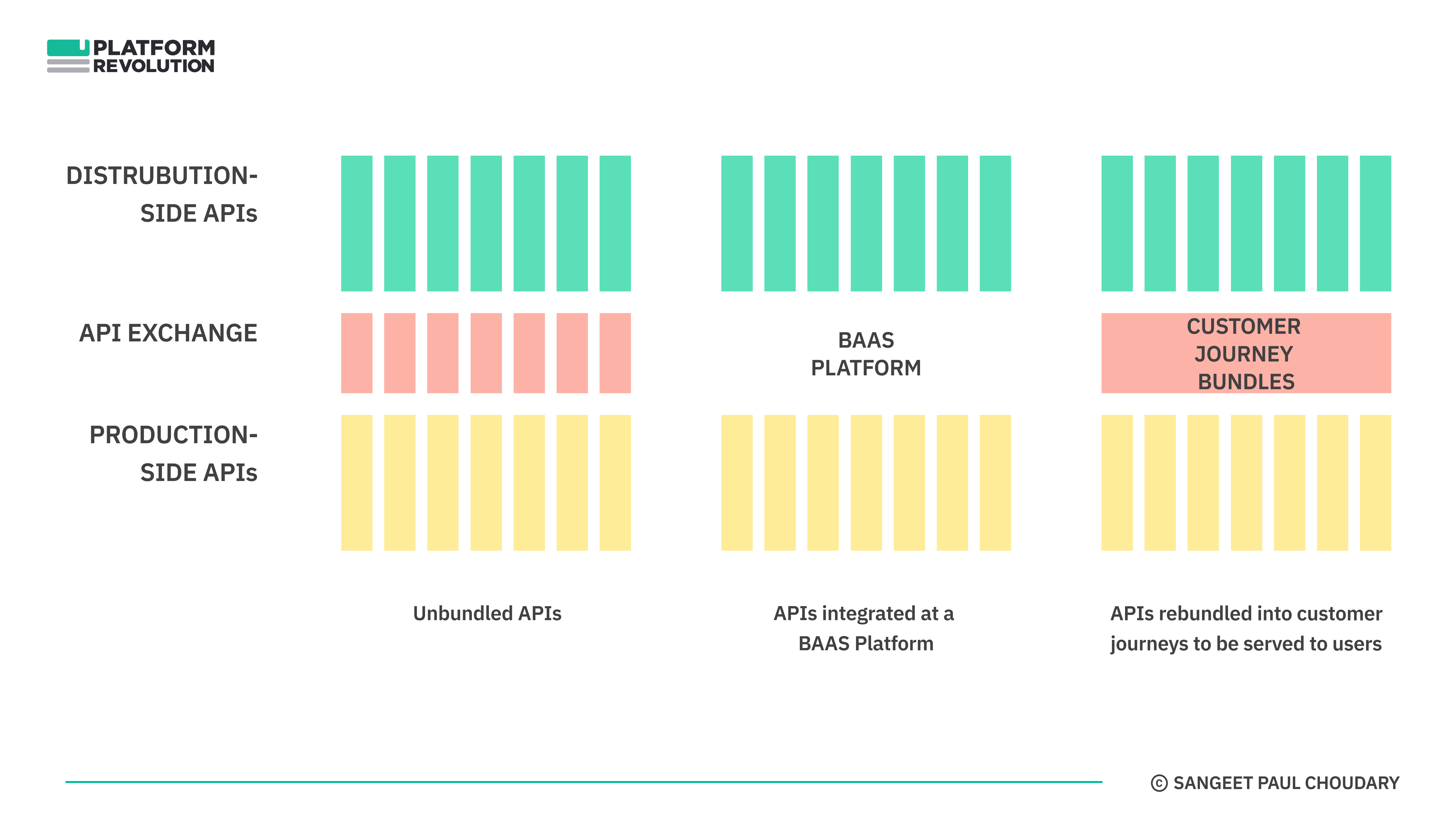

As I point out in The financial services value stack:

The API exchange layer - typically referred to as Banking-as-a-service (BAAS) platforms - manages interactions across the financial services stack. On one hand, this layer aggregates product provisioning APIs across the financial services production ecosystem. On the other hand, it integrates across websites, apps, and other digital services in the consumption ecosystem, providing them access to these APIs.

With every bank provisioning its product as APIs, players at the API exchange layer manage the aggregation and provisioning of these APIs across multiple banks.

This sounds simple enough.

Aggregate production side APIs (inputs) on one side and integrate with consumption-side APIs (distribution) on the other, and create a one-stop integration layer.

Yet, most BAAS ‘platforms’ are merely glorified distributors. They are not platforms.

The power in the value chain remains with the banks provisioning APIs. The more concentrated the banking provider side, the lower the power with the intermediary - in this case the Banking-as-a-service platform.

Neither the inputs nor the distribution are proprietary. Any competing integration provider can also aggregate the same APIs.

In order to win at open banking, BAAS platforms need to migrate value and power to their layer through rebundling.

As I explain in Finding the product in your platform:

The BAAS platforms that eventually win are the ones that are able to create ‘products’ at the point of rebundling. These ‘products’ are carefully crafted consumer journeys, typically created by:

taking production-side APIs as input,

wrapping them in core banking capabilities to make the APIs consumable by third-party non-banking entities, and

rebundling them into a consumption-side customer journey.

BAAS platforms win when they develop deep customer insight into consumption-side journeys at their partners (e.g. buyer journey at an e-commerce store) and carefully curate the most relevant production-side APIs into that bundle.

You will note again, that much like the innovation ecosystems of vehicle data and the playlists of Spotify, rebundling helps you gain power in the value chain, particularly in value chains where the production side is highly concentrated.

How do intermediaries win?

Not all intermediaries are platforms. Some are glorified distributors.

In fragmented markets, intermediaries with through aggregation. They resolve search costs.

But in concentrated markets, aggregation doesn’t hold the same value.

In such markets, intermediaries win through rebundling inputs from producers.

Even in fragmented markets where multiple platforms play as aggregators, rebundling is an effective way to differentiate one platform vs the other.

Eventually, power accrues to the point of rebundling.

Hi Sangeet,

As an open banking aggregator, we re-bundle our user's transaction data and give people back their monthly carbon footprint or lifestyle emissions. We then provide brand recommendations to help them lower it.

As a marketplace, we incentivize people with green cashback and green loan deals to help bridge the gap towards price parity between 'incumbent non-green, typically lower priced' products & services and 'low emission, typically premium priced' products & services.

Our filter is an external third party that validates whether a product is sustainable or is just greenwashing.

Bridging the gap in income inequalities plays an important part in tackling climate because if you can't afford to care, why would you? But when 55% of the cumulative emission reductions required to stay on track for 2050 come from consumer choices, it's an opportunity the world can't afford to miss.

You are right, as an intermediary, anyone could copy our BaaS plumbing and then build a recommender system and provide a curated 'playlist' of what they should buy to lower their lifestyle emissions.

So it begs the question, how (else) should we re-bundle our product to create value?

As I start to think about defensibility, I keep coming back to the idea of the credit score. We are all used to getting our credit score and paying 3 USD to Experian or Dunn & Bradstreet. Credit scoring is essentially a measure of abundance, as in, what loan, mortgage, or overdraft can I get access to? What we are trying to re-bundle is a measure of 'ecological abundance' or simply put, how much time have we got left before runaway climate change makes life as we know it irretrievable. Sadly, if people only find value in their carbon footprint when water starts coming under their door, it will be too late.

It comes down to a matter of intrinsic value versus extrinsic value and whether people have the empathy required to value something that is not immediately of benefit to them in the short term. After all, no one wakes up in the morning and says "I know, I'm going to buy something sustainable today."

So would people be willing to pay 3 USD a month for their carbon footprint? Newly published robust research suggests that people are willing to pay 1% of their income for the climate issue to just go away. So in that sense, what's a few bucks per month?

In Platform Scale you unpack the various platform interactions such as value units, filters, and currency. And money - whether fiat currency or otherwise - will always be how we exchange value. And since our carbon footprints don't have any everyday value, as such, because it's not a metric we need to get through the month (i.e. it doesn't pay the bills, rent, or mortgage) it means that it will never be a currency.

It is not a filter either because access to consumerism is unlimited and our carbon footprint is not capped or regulated from the top down. That is, of course, the problem because within a few clicks, we can order whatever we want and fly wherever we want. So, as you can probably gather, we are trying to apply platform thinking to create ground-up value and awareness.

I would love to get your and the community's thoughts on where the carbon footprint (credit score) sits on the platform canvas. Climate fintech is important as it allows us to redo the plumbing of our economy. I haven't read much of your new material on Web 3, but road testing on the Web 2.0 API economy and then bridging the finished product to Web 3.0 sounds like it could be viable.

Arguably, our monthly carbon footprint (credit score) is the underlying yardstick by which we should measure the economic value and economic progress more generally; as let's face it, growth - as we know it - can't go on forever.

Either way, our economy is overdue an upgrade so we might as well call it capitalism 2.0 as that's the wave upon which we must ride out change. It's probably too late in the day for system change on a grand scale so let's stick with what we've got.

For consumers, sustainability is increasingly the final tick-in-the-box for how we decide whether to buy something (or not) but it's not the primary driver and never will be.

Anyway, please take a look at what we've built on climatesavers.io (not optimised for mobile yet)

https://vimeo.com/917544024

Your feedback and ideas would be appreciated. Do let me know if you ever come back to Amsterdam as it would be great to meet you again.

Rory